A cikk eredetileg magyar nyelven jelent meg, itt tudjátok elolvasni.

The Hungarian parliamentary election on 12 April 2026 delivered a two-thirds majority for the Tisza Party. Whitereport, the media market data and advisory firm, shared with Kreatív a fact-based quick analysis of the media and advertising market, together with the first questions it believes demand attention.

The Whitereport database, which was launched with data from 2010, has since tracked the factual landscape of media supply, commercial activity, ownership and finances. It now provides a long-running view of structural change across more than 12,000 media outlets and platforms, as well as more than 1,000 publishers and media operators.

The annual Whitereport for Directors report offers a detailed analysis of domestic and international media and advertising market conditions and trends.

The past 16 years

This section reviews the main developments of the past 16 years through three lenses: market effects, government measures and EU actions. Each has shaped the Hungarian media and advertising market in important ways.

A. Market effects

- Media consumption habits have changed significantly in favour of online channels. Yet while domestic online news sites together reach 2.5 million people a day, Google reaches more than 3 million, and Facebook and YouTube each reach more than 1 million EDMA-NMHH, March 2026. These platform effects are prevalent in orienation worldwide: in Hungary, 43 per cent of the population gets news from Facebook and 27 per cent from YouTube Reuters Institute, 2024.

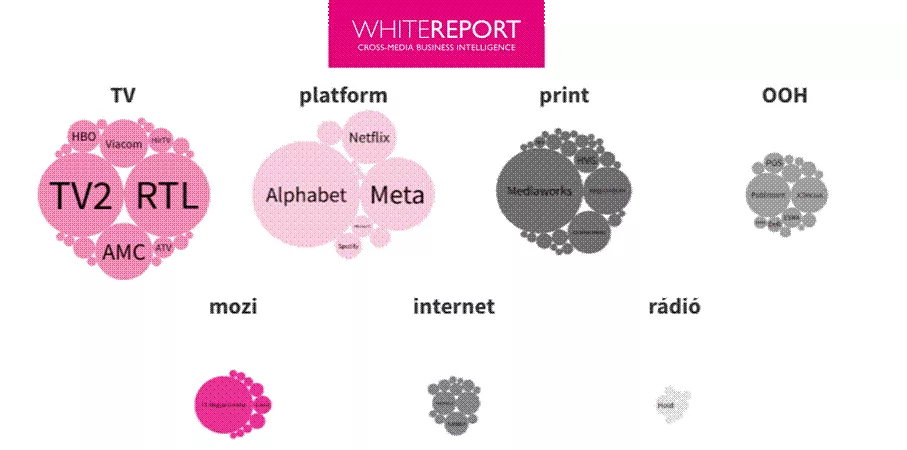

- The media and advertising market is no longer simply cross-media, as it was in the 20th century, but operates as a far more complex media-platform ecosystem. Several online platforms have become global monopolies, or, in EU terms, hold significant market power, while domestic media supply remains fragmented, with 12,000 outlets and more than 6,000 media operators active in Hungary [Whitereport].

- Advertising spend has shifted decisively towards digital. Online accounted for 56 per cent of net-net advertising spend in 2024, up from 10 per cent in 2008. In 2025, online platforms accounted for 36 per cent of total advertising spend [MRSZ].

- The growth rate of platform advertising spend (CAGR), is far higher than that of traditional media. Between 2010 and 2025, average annual advertising spend growth was 5 per cent for traditional media, compared with 22 per cent for platforms.

- Looking at total annual net revenues for media companies, including advertising, distribution and other income, the CAGR for traditional media companies was 2.6 per cent between 2010 and 2024 [Whitereport, based on top 100 media company time-series data].

- Competition between global platforms and media companies is also evident in distribution revenues. Since the digital switchover, national commercial broadcasters have been able to benefit from revenue, which reached HUF 78 billion in 2025 [MEME]. But subscription-based global streaming services, such as Netflix, have created a new competitive reality. Whitereport estimates that streaming revenues may now exceed half of linear TV distribution revenues.

- Data is the new value. The data assets of online platforms have made personalised advertising — and personalised content — possible, with content providers also contributing to that value. Yet platforms do not share the revenue generated by advertising with the content providers whose content and credibility help create it. This is the so-called value gap, or value transfer, which emerged with the rise of digital platforms. Although EU rules have created the legal basis for this in Hungary too, in 2024 the market still failed to enforce publisher neighbouring rights — the royalties payable by global platforms to content providers — through collective rights management, with the exeption of a few individual agreements: Repropress tariffs: The ministerial decision still favours global platforms over domestic publishers.

- International media companies have been gradually pulling out of Hungary, and the region more broadly. In the early 2010s, partly because of the global financial crisis and Hungary’s then economic position, international media investors began to withdraw from the country and/or the region. Whereas foreign ownership accounted for 78 per cent of the top 100 media companies’ total revenues in 2010, that figure had fallen to 35 per cent by 2025 [Whitereport data].

- As domestic media ownership increased, the share of pro-government private ownership also rose significantly, through figures such as Simicska, Vajna and Lőrinc Mészáros. This was a gradual and well-documented process, closely followed by the press.

- With the loss of Hungary’s former regional role, our regional leadership positions were lost too — along with our competencies: MRSZ-EY, 2024.

- We entered the genAI era at the end of 2022. By the end of 2025, ChatGPT had become the world’s fifth most visited website, and in Hungary it now draws daily traffic comparable to a mid-sized website EDMA-NMHH, March 2026. It is therefore becoming an increasingly important factor in the battle for audience attention.

- genAI platforms are drawing more and more traffic away from publishers, brands and other content providers through the zero-click phenomenon. The new value gap in the AI era is that genAI platforms do not pay for training their models on publisher content, nor for the ongoing use of that content.

Overall, between 2010 and 2026, the platform era entered a mature phase, becoming indispensable both in audience reach and in revenue generation. Media companies, agencies and advertisers now have to operate in this new cross-media, platform-driven market reality, while the slow pace of regulatory change continues to leave content providers and platforms under a double standard that favours the latter.

B. Government influence

Focusing on the economic and structural dimensions of the media market, the following developments took place between 2010 and 2026 under four Orbán governments.

- From 2010 onwards, the centralization of public service media and the increase of its budget began.

- An advertising tax was introduced 2014. XXII., later amended in 2017 with different tax rates ranging from 5.3 to 7.5 per cent, applied to actual advertising revenue above HUF 100 million. The current rate is 0 per cent. As we noted in a public analysis in 2015 (here) — and in several publications since — media company profit margins under normal market conditions tend to sit between 5 and 8 per cent, which means that if advertising makes up only half of a company’s revenue, the tax can absorb a substantial share of profit. Based on factual data from the past 16 years, as many as one third of media companies have been loss-making.

- State advertising spend has been centralised at the National Communications Office since 2014 (Government Decrees 247/2014 and 162/2020). Of the HUF 416 billion advertising market in 2025, roughly HUF 70 billion may have been state spending — around 17 per cent of total spend. HVG report.

- Government-tied interests are present across the entire advertising value chain, not only as advertisers through the National Communications Office, but also via agencies, service providers and media owners.

- The so-called bonus law was introduced in 2015, amending the Advertising Act of 2008. It guarantees agencies a 15 per cent commission, far above the global market average of 2 to 5 per cent, and thus suppressing competition between agencies: The advertising market is now effectively state-priced.

- The Central European Press and Media Foundation (KESMA) was established in 2018 by Government Decree 229/2018 (XII.5) as a “strategically important merger” without Competition Authority review. Many media companies transferred assets into the foundation after coming under domestic and pro-government ownership. Mediaworks, Hungary’s largest media company, operates under this foundation structure, with annual net revenue of HUF 56 billion in 2024. Other assets donated to KESMA include Hold Rádió, operator of the only national commercial radio station, Retro Rádió, as well as HírTV and several others. Altogether, these companies generated roughly HUF 70 billion in annual net revenue in 2024, according to Whitereport data.

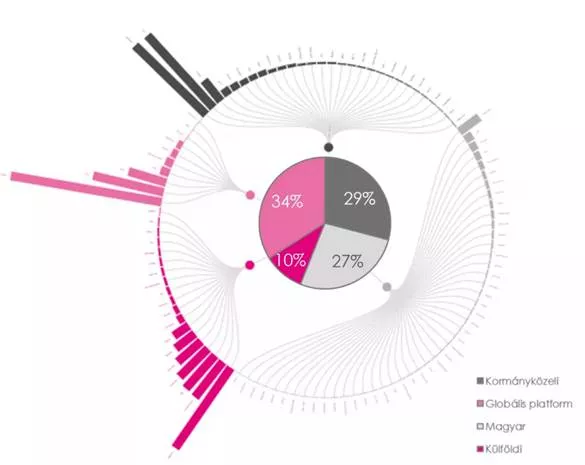

- The share of revenues attributable to pro-government interests rose from 13 per cent to 50 per cent between 2010 and 2025, excluding public media budgets. Of the top 100 Hungarian media companies, 39 were government-tied in 2025 [Whitereport].

- As a result of politically motivated acquisitions, media outlets with significant economic value have ceased to exist (e.g. Népszabadság, 2016), or have been removed from the competitive market (see KESMA). At the same time, so-called economic miracles also appeared — for example, Netrise, which reportedly achieved a 90 per cent profit margin on HUF 3 billion in turnover through its sole Femina.hu site — while the typical profit margin for media companies remained between 5 and 8 per cent, according to Whitereport Financial time-series data.

- Through the Sovereignty Protection Office, funding for non-profit media has been restricted to domestic sources. Whitereport data show that more than 1,500 associations or foundations operate media outlets, typically within the long tail — around a quarter of all operators.

Overall, alongside market transformation, government measures have also shaped the media and advertising market structurally and financially. Media has become a strategic sector for the government.

C. EU actions

To curb the dominance of global platforms and increase competition, the EU started regulatory preparations from 2010 onwards, followed by new legislation as part of the adaptation to a borderless digital world. To highlight some of the most important elements.

- The GDPR was designed to strengthen the fundamental rights of individuals to the protection of personal data and to create a unified framework for the free flow of data within the EU. This regulation, which directly affects the online advertising market, has so far failed to reduce the competitive advantage of platforms.

- The CDSM Directive, or Directive (EU) 2019/790 on copyright and related rights in the Digital Single Market, aims to modernise copyright and neighbouring rights in the digital single market, particularly in relation to online content-sharing, the protection of press publications and fair remuneration for rights holders.

- The DSA-DMA package is the EU’s comprehensive regulatory framework for digital platforms. The Digital Services Act is intended to create a safer and more transparent online environment through common EU rules on illegal content, platform responsibility and the protection of users’ fundamental rights online. The Digital Markets Act aims to deliver a fairer and more competitive digital market by regulating the behaviour of so-called gatekeeper platforms and preventing abuses of market power.

- The AI Act is designed to ensure the use of safe, trustworthy artificial intelligence systems that respect fundamental rights within the European Union, through a risk-based regulatory approach.

- The European Media Freedom Act aims to strengthen media freedom and media pluralism at EU level, protect editorial independence, increase transparency around media ownership, and set requirements for assessing media market concentration and the allocation of state advertising.

Overall, alongside the continued modernisation of sector-specific legislation, the EU has focused since the second half of the 2010s on regulating platforms and reducing competitive disadvantages through digital legislation.

Where we stand now

As Whitereport’s earlier analyses have also shown (e.g. on Kreatív here), the media and advertising market is a complex structure in which four main segments compete on the supply side: foreign-owned media companies such as RTL and AMC; Hungarian-owned media companies such as Telex.hu Zrt. and Central Media; government-tied media companies such as Mediaworks and TV2; and global platforms such as Google and Facebook.

From a market-structure perspective, one striking fact is that the top 100 media companies account for more than 90 per cent of revenues, according to Whitereport data, yet there are still more than 900 micro-companies operating Hungarian-language television, radio, print and online outlets. Ninety-eight per cent of print and online media are domestically owned, as is 100 per cent of the radio market. In practical terms, that means there has been very little inflow of foreign capital or know-how into these segments through ownership. It is into this complex media-market reality that the new government steps in during 2026.

What comes next

Whitereport raises a series of important economic and structural questions for the new era, without claiming to be exhaustive.

- What will happen to the financial measures introduced under the Orbán governments, such as the advertising tax and the bonus law?

- What will happen to the National Communications Office as the centralised body for purchasing advertising services? Will there be genuine competition in state media planning, buying and other advertising tenders?

- What will happen to KESMA? Will the media companies offered as donations (which operate in several separate companies) be privatized from the foundation form?

- Will there be a review by the Competition Authority, e.g. on the KESMA concentration, or perhaps on the issues of the Ringier acquisition?

- How will the scale and distribution of state advertising spend change — and if it falls, what will that mean for market competition?

- How will the public media budget develop, and will audience figures rise as a result of editorial changes?

- What will happen to the supplier ecosystem built around the National Communications Office — media and advertising agencies, sales houses and the rest of the value chain?

- If Hungary receives EU funds again, what impact will that have on consumption, and on advertising and media spending?

- Will the new situation affect business models — for example, the willingness to donate to news sites?

- Without low levels of foreign capital and expertise, can Hungarian-language content providers remain competitive?

- Can professional advocacy organisations become more active? Will there be dialogue between the new government and sector associations on advertising and media issues?

- What will the new government’s EU policy look like, particularly on media and platform issues?

- Can support be expected for the competitiveness of content providers, for example through the introduction of publisher neighbouring rights?

- Will the mindset of the advertiser market shift towards innovation and new solutions, and can Hungary keep pace with international markets and improve its position rather than continuing to drift into isolation?

There are many open questions, but one of the most important macro-level issues is whether the Tisza Party’s victory can trigger a genuine positive shift, and whether the media and advertising market can now move into a new phase of development.

Kinga Incze, Founder and CEO of Whitereport and Mediaspace.global, draws attention to the following: “The Hungarian media market must be viewed in the context of the platform era and the age of AI. Alongside a review of earlier government measures, there is a need for a forward-looking, innovation-friendly approach that supports the competitiveness of domestic players and is based on market knowledge and professional dialogue. Of course, the market itself must also be a partner in this, and cooperation between market players also needs to begin.”

Kiemelt kép: Adobe Stock